Since Ronald Reagan’s 1981 Executive Order 12291 established benefit-cost analysis as standard practice for major rule changes, benefit-cost analysis has been commonly used to assess the efficiency of proposed federal regulations. Because of this and subsequent executive orders, all federal regulations that are projected to have a total economic impact of over $100 million are subject to a full benefit-cost analysis. Despite this prevalence at the federal level, benefit-cost analysis is much less common at the state level. In 2013, the Pew-MacArthur Results First Initiative released a study of the use of benefit-cost analysis in the states (study results were subsequently reported in the Journal of Benefit Cost Analysis in 2015). The study found that, over the four years from 2008 to 2011 states conducted only 36 full cost benefit analyses and 312 partial cost-benefit analyses. This averaged out to 9 full analyses and 78 partial analyses per year across all 50 states.

Since that study, the Results First Initiative has worked to outfit states with the capacity to conduct benefit-cost analyses, replicating cutting-edge work done by the Washington State Institute for Public Policy, the leading state producer of benefit-cost analyses. Despite these and similar efforts, benefit-cost analysis is still relatively rare at the state level.

Scioto Analysis is an Ohio-based policy analysis firm working to improve the quality of policy analysis in state and local government. To create a baseline for assessing the quality of policy analysis in the state of Ohio, we decided to replicate the methods of the 2013 Results First study, but looking specifically at Ohio’s use of benefit-cost analysis from 2012 to 2018. The resulting study, “Cost-Benefit Analysis in Ohio: Building State Policymaking Infrastructure,” was released last month.

We followed the Results First approach by collecting data in three phases. We first sent a survey to 30 state agencies and think tanks (independent policy research organizations) asking them for benefit-cost analyses and similar studies, then scanned the websites of these agencies and think tanks to locate additional publicly-available studies that were posted online. Afterwards, we interviewed half a dozen researchers in Ohio who had conducted analyses to glean insights into the impact of these studies on policymaking in the state.

We followed the definition of benefit-cost analysis from the 2013 Results First study. The original study defined a benefit-cost analysis as a study that comprehensively measures direct and indirect costs, monetizes tangible and intangible benefits to the extent possible, measures program costs and benefits against alternatives or a baseline, discounts future costs and benefits to current year value, discloses key assumptions used in calculations, and conducts sensitivity analysis.

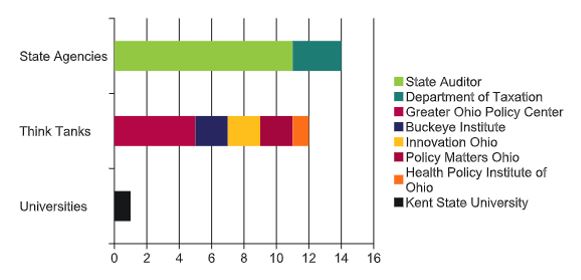

The topline finding of the study was that benefit-cost analysis in Ohio is extremely rare. We were unable to find a single study conducted during the past seven years that included all the above characteristics. We were, however, able to identify 27 studies that at the very least assessed direct costs and measured outcomes (see Figure). These “partial cost-benefit analyses” were deemed “notable analyses.” These notable analyses were spread across a range of policy areas, with economic development (7), health/social services (6), and transportation (5) receiving the most attention. These analyses were also split fairly evenly between state agencies (14) and independent think tanks (12). The 11 performance audits conducted by Ohio Auditor of State made up the majority of agency analyses. The 12 notable analyses identified by think tanks were conducted by five different organizations.

Notable Analyses By Organization Type

In addition to studying benefit-cost output, Scioto also performed a review of Ohio’s policy analytic infrastructure. Although the data from this analysis is descriptive and should not be considered causal or even correlative, it is nonetheless valuable as a snapshot of Ohio’s policy analysis infrastructure.

Ohio is home to 26 think tanks and 3 top research universities. Ohio has fewer think tanksper capita than any of its neighboring states (as indicated in the table from our study) and also has fewer top research universities per capita than these states. Its legislature has 476 full-time staff, which may seem large on its face, but on a per-capita basis puts Ohio below all of its neighboring states except Indiana. Further research is warranted to better establish how these indicators impact the quantity and quality of analysis in a state, but these data points suggest that Ohio has less capacity for analysis than its neighboring states.

Ohio also has state institutions that provide partial cost data to policymakers. Its state legislative research organization, the Ohio Legislative Service Commission, provides state accounting cost estimates on all bills that receive a second committee hearing and its regulatory review process requires an analysis of the cost of proposed regulations to private firms in the state. These institutions provide a foundation on which benefit-cost practices could be built.

The report concludes with recommendations for state and private actors interested in improving analysis in the state, including increasing the number of research universities and think tanks in the state, improving analyst training, and incorporating benefit-cost analysis into legislative and agency processes. For Scioto’s part, we will be conducting demonstration benefit-cost analyses later this year to show how benefit-cost analysis can be carried out at the state level. We also will release a state-specific handbook for analysts in the state interested in an introduction to benefit-cost analysis. The state has a lot of work to do, but with a few institutional tweaks, Ohio could be among state leaders in the use of benefit-cost analysis.