On Balance: How Expanding Health Insurance Coverage Reduces Financial Risks

When researchers and policy analysts consider the benefits of expanding health insurance coverage, they understandably focus first on the health benefits, such as reduced infant mortality, increased longevity, lower rates of illness, and improved quality of life. However, access to insurance also lowers financial risk exposure—i.e., it protects the household against major shocks to its financial well-being—by mitigating lost earning capacity and helping to cover out-of-pocket health care expenditures. This post describes a new article published in the JBCA, Valuing Protection against Health-Related Financial Risks with co-authors Kalipso Chalkidou and Dean Jamison, which is part of an open access Special Issue, Conducting Benefit-Cost Analysis in Low- and Middle-Income Countries, edited by Lisa Robinson (Harvard T.H. Chan School of Public Health).

We suggest that any assessment of expansions or reforms in health insurance programs should account for these financial effects; indeed, they could even have a larger impact on the overall welfare of lower-income households than the health effects alone. In our study, we provide several practical approaches to measuring these effects to assess both financial benefits, as well as distributional changes in income inequality arising from the health insurance expansion. We follow earlier literature in using a simple two-period model of the household, where welfare is calculated based on a conventional expected utility framework.

To illustrate our approach, we consider a hypothetical low and middle income country (LMIC) to illustrate how observed financial factors could be implemented in a benefit-cost analysis. Suppose there are two income groups, those with incomes of $1,000 in US dollars (80% of the population), and those with incomes of $4,000 (20% of the population). Consumption is equal to income for the low-income group, and slightly less than income for the high-income group. We assume an expansion of the existing insurance system that will increase per-capita spending by $70; this is fully funded by an increase in user fees or tax payments of $50 for the lower income group and $150 for the higher-income group.

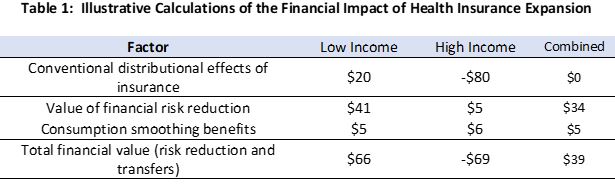

The first row of Table 1 illustrates the conventional financial impact of this insurance expansion; lower income households receive a net gain of $20 ($70 in expected health benefits minus $50 in extra user fees or taxes) while high-income households lose $80 ($70 in expected health benefits minus $150 in additional user fees or taxes). As expected, this conventional financial accounting of a fully funded health insurance program yields a net impact of zero; some people pay in, while others pay out. As a first step, this is a useful exercise – to document the distributional effects of who benefits, and who loses – from the insurance expansion. In the example here, we assumed that both high- and low-income households expanded health care use by the same amount ($70), but it could be that because high-income households live closer to new health facilities (for example), they could benefit by more than low-income households, as in one study from the World Bank. In that case, it’s possible that the net distributional effects could be regressive.

But this calculation ignores two additional effects of the insurance policy. First, health insurance pools the risk of unexpected medical expenditures between healthy and sick households. Using illustrative parameters of risk aversion, coverage, and catastrophic health risks, we estimated the impact of the risk reduction – that insurance pays in the unhealthy state of the world – on household welfare. The value of insurance is greatest for low-income households, so the dollar benefit (in addition to the $20 subsidy) for this group is $46, while the high-income household also benefits, but less so ($5) given that they have their own resources to guard against such risks; the social benefit, $34, takes the weighted average of the two income groups.

Second, health insurance premiums and tax payments paid at an earlier age can smooth out consumption over time, particularly in the presence of “hyperbolic discounting” or when people have trouble saving for the future and consume nearly all their income today. Table 1 provides estimates of these benefits, which in this example are conservatively estimated at $5 for lower-income and $6 for higher-income households. (This latter group may benefit more in dollar terms given their higher levels of consumption and tax or premium liabilities.) That is, since health shocks often come towards the end of life, paying early-on through payroll contributions, for example, helps to lessen the shock of having to scale back on consumption later in life.

In sum, our adjusted financial benefit measure yields a considerably more progressive (and net social gain) estimate of the non-health benefits of health insurance, with more than triple the monetary benefits to lower-income groups ($66 versus $20), and a slightly smaller decline financial for the higher-income groups (-$69 versus -$80).

It is important to note that these benefits presented in Table 1 should be considered illustrative; more generally the magnitude of the benefits or costs will depend on the product design and will include more than just two income groups. For example, in some countries health care expansion may occur by building tertiary hospitals in urban areas; in that case one would want to capture different benefits for urban and rural households as well as considering benefits by income. One should also consider the impact of the reform on the income of health care providers, who may also benefit from the expansion. Finally, there may be additional value if for example the government implements large-scale purchasing of health care supplies at lower costs.

Regardless of the specifics, the major point of this article is that for any assessment of health insurance reform, that there should be a careful consideration of the financial benefits of health insurance that arise from the mitigation of financial risks, and the potentially large distributional consequences of how the program is financed. Each country will face its own specific challenges in creating and expanding health insurance coverage, but our hope is that this simple framework will allow policy makers to provide a more accurate and equitable description of the benefits arising from health insurance expansion.